The $17 Billion Tell — D2D Spectrum, Read From September 2025

A backtest: frozen the day after SpaceX bought EchoStar's spectrum, four structural calls on who buys the constraint next — scored against what actually happened, control included.

Method-calibration backtest · vantage 2025-09-09 · blind re-derivation 2026-06-08

A backtest: scored history, not a live call. This freezes a vantage at September 9, 2025 (the day after SpaceX agreed to buy EchoStar's spectrum), derives every call from only what was knowable by that date, and scores it against what actually happened. It calibrates our method in public; it is explicitly not a forecast you can act on today, and it is a separate piece from the live direct-to-device issue on AST SpaceMobile. We report backtest scores in their own lane, away from the live record, and we show the un-flattered number. Hindsight is undefeatable, which is exactly why the honest Brier, not a cherry-picked one, is the point.

The Call (as of 2025-09-09)

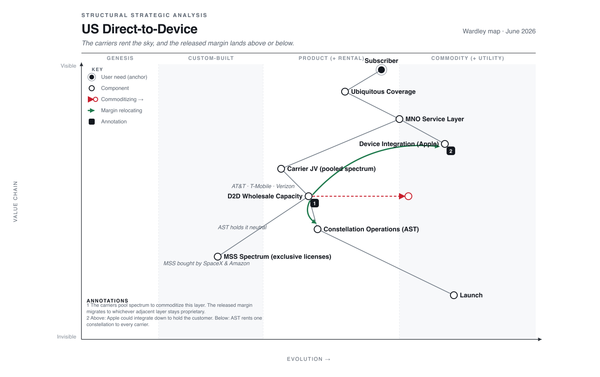

Direct-to-device means an ordinary phone reaching a satellite where the towers end, no special hardware in your hand. The scarce input under it is not rockets or satellites, both of which you can build more of. It is licensed mobile-satellite spectrum: airwaves a regulator has tied to satellite use, capped by law, impossible to manufacture. Yesterday SpaceX agreed to pay about $17 billion for EchoStar's slice of it. That price is the tell. It is the first public mark on the asset class, and it sets two different chains in motion that a single lens would blur together.

The first chain is about who gets bought. We bet the takeover premium attaches not to spectrum as such but to spectrum already fused into a mass-market device ecosystem, which points at one name on the board: Globalstar, the backend behind Apple's iPhone satellite SOS. A capital-rich platform, Amazon the leading candidate, takes it by acquisition rather than renting through a carrier, while the carriers stay tenants. The second chain is about what reprices, and it is where we set a trap for our own logic. A control call says the re-rating spreads to an uncospecialized holder, Iridium, that our discriminator says should stay flat. We expected that one to miss. The scope is the US market: US carriers, US-licensed satellite spectrum, US regulator. Four calls, blind confidences from 40% to 73%, scored against the record.

The Situation (vantage facts only)

Dated facts available by 2025-09-09. Analysis after.

- 2022-09: Apple launches Emergency SOS via satellite on the iPhone 14, running on Globalstar capacity; the bulk of Globalstar's network is contracted to Apple. Spectrum fused into a mass-market device (Apple).

- 2023-11-03: Qualcomm ends Snapdragon Satellite with Iridium, stating that smartphone makers prefer standards-based connectivity over the proprietary architecture. Iridium loses the smartphone seam (Via Satellite).

- 2024-03: The FCC adopts the Supplemental Coverage from Space framework, standardizing the regulatory interface for D2D (FCC 24-28).

- 2024-11-01: Apple commits about $1.5B to Globalstar for a new constellation; Globalstar allocates 85% of network capacity to Apple. The single-anchor lock deepens (CNBC).

- 2025-03 → 06-13: AST SpaceMobile secures long-term access to up to 45 MHz of Ligado L-band spectrum for D2D, with $550M+ in payment obligations. Even a carrier-partnered entrant pays heavily for spectrum control (BusinessWire).

- 2025-04: Amazon launches its first production Kuiper satellites against an FCC milestone requiring half its constellation deployed by 2026-07-30; Kuiper holds no satellite spectrum and has announced no D2D offering. A capital-rich fast follower on a hard clock, missing the cospecialized asset (Spaceflight Now).

- 2025-05: FCC Chairman Carr opens inquiries into EchoStar's spectrum utilization after SpaceX complained it was warehousing the licenses; EchoStar misses interest payments and warns of $114M+ due July 1. The regulator is forcing idle capacity to market (EchoStar 8-K).

- 2025-07-23: T-Mobile's T-Satellite (Starlink direct-to-cell) launches commercially at about $10/mo, offered to AT&T and Verizon customers too. A carrier takes a tenant position on a rival's constellation (Broadband Breakfast).

- 2025-08-26: AT&T agrees to buy EchoStar's terrestrial spectrum (600 MHz and 3.45 GHz, ~400 markets) for about $23B all-cash, no satellite spectrum. Carriers deploy capital on terrestrial airwaves, not the satellite layer (EchoStar 8-K).

- 2025-09-08: SpaceX agrees to buy EchoStar's AWS-4 and H-block satellite spectrum for about $17B, plus a long-term commercial agreement and a next-gen Starlink Direct to Cell. The trigger: the leader pays to elevate the constraint (PRNewswire).

The Mechanics

The prime mover, and the order of what follows. Read the dates as a sequence, not a snapshot. SpaceX's $17B is the move that starts everything else. Before it, the asset class had no public price; book values sat far below what exclusive licensed spectrum was worth to a platform. After it, every other player is reacting to a number on the table. The carriers' pooling, the repricing of comparable holders, the scramble to buy what's left: all of it is downstream of the leader marking the constraint. Naming the prime mover matters because the easy mistake is to read each reaction as its own independent event. They are one chain. The $17 billion tell sets the price; everyone else responds to the mark.

Bottleneck: the leader priced the constraint, and pricing a thing forecloses it. D2D's binding input is licensed satellite spectrum, fixed by law, not by cost. When the leader buys the constraint outright, two things happen at once. The remaining supply gets scarcer, and the price of the remaining supply is now public. Goldratt's move is to elevate the constraint by acquiring it; SpaceX did exactly that, and in doing so it published a mark every other holder is now valued against. Mechanism: the tell is a price, and a price both scares off rivals and reprices the comparables.

Modularity and integration: who buys is decided by cospecialization, not by spectrum alone. Here is the discriminator the whole backtest turns on. D2D is still not-good-enough, so integrated stacks win and the takeover premium should attach to spectrum already fused with a mass-market device ecosystem, not to a raw license. That is the difference between Globalstar and Iridium. Globalstar's bands run Apple's iPhone SOS; its spectrum is cospecialized with the largest device ecosystem on earth. Iridium's proprietary architecture lost the smartphone seam when Qualcomm walked in 2023. So the lens picks Globalstar as the target and ranks Iridium below it, and a capital-rich platform that prices connectivity as an ecosystem complement, not as telco coverage insurance, is the natural buyer. Mechanism: the $17 billion tell sets the price, but the takeover premium lands only where the spectrum is already fused to a device ecosystem.

Unit economics: the same mark that picks the buyer also reprices the bystanders. Run the tell through a valuation. Revenue in D2D scales with licensed spectrum under exclusive mobile authorization, the throughput per unit of the constraint, not with the number of satellites. The SpaceX price sets a public mark on that unit far above where the holders traded. Once that mark exists, the sector-scarcity story can lift any spectrum holder's equity, cospecialized or not, because the market reprices the asset class before it sorts the targets. This is the seam where our own logic could break. Cospecialization governs who gets bought; it does not obviously govern what re-rates. We built the control call to find out. Mechanism: the tell reprices the asset class first and sorts the cospecialized targets second, and the gap between those two is where the control fires.

The Predictions (blind vantage confidences)

1 · A hyperscaler secures control of satellite spectrum

Within 12 months (by 2026-09-09), a platform, Amazon the leading candidate, secures control of mobile-satellite spectrum by acquisition, controlling stake, or exclusive long-term rights, rather than entering through a carrier partnership; the likeliest route is acquiring Globalstar.

Confidence 62% · Horizon 2026-09-09 ·✓ HIT 2026-04

Wrong if: by 2026-09-09 no hyperscaler has announced an acquisition of, controlling stake in, or exclusive long-term usage rights to MSS spectrum with US authorizations — i.e., the entrants take carrier/wholesale partner positions or stay out.

2 · Globalstar is acquired at a steep premium

Within 18 months (by 2027-03-09), Globalstar is acquired, or receives a public acquisition or controlling-stake offer, at a premium above 50% to its undisturbed price, with the pricing anchored by the SpaceX $/MHz-POP benchmark.

Confidence 66% · Horizon 2027-03-09 ·✓ HIT 2026-04

Wrong if: by 2027-03-09 no acquisition or controlling-stake offer for Globalstar at >50% premium to undisturbed price has been made public.

3 · Carriers stay tenants, they don't buy

Through 2026-09-09, no major US carrier (AT&T, Verizon, T-Mobile) acquires control of satellite spectrum or a D2D operator; the carriers take tenant and wholesale positions on constellations owned by others.

Confidence 73% · Horizon 2026-09-09 · open, trending hit

Wrong if: by 2026-09-09 any of AT&T, Verizon, or T-Mobile announces acquisition of MSS spectrum licenses, a satellite D2D operator, or a controlling stake in one.

4 · The re-rating spreads to Iridium (the call we expect to lose)

Within 12 months (by 2026-09-09), the constraint repricing extends to satellite-spectrum holders generally: Iridium re-rates more than 50% above its undisturbed 2025-09 level or becomes a disclosed acquisition target. We expect this to miss: cospecialization, not spectrum as such, should carry the premium, and Iridium lost the device seam in 2023.

Confidence 40% · Horizon 2026-09-09 · open, control fired — trending hit

Wrong if (it hits): by 2026-09-09 Iridium has either re-rated >50% above its undisturbed 2025-09 share price or been the subject of a disclosed acquisition approach.

What really happened, scored against the record. Both resolved calls hit, fast. Amazon agreed to acquire Globalstar for about $11.6B on 2026-04-14, the named target and the named route, seven months into a twelve-month horizon, with the Apple satellite relationship folded into the deal: the cospecialization reading confirmed, the asset's value was its device fusion (call 1, CNBC). The premium ran to about 117% against the >50% bar, and the equity had re-rated months before the announcement, a leading signal faster than any regulatory filing (call 2, Bloomberg). Call 3 is trending hit: the Globalstar buyer was a platform, not a carrier, and the 2026 tri-carrier D2D JV pools spectrum and rents rather than buying an operator.

The control fired, and that is the finding. Call 4 was built to miss, and it did not. By June 2026 Iridium had re-rated about 193% year-to-date on an explicit "spectrum optionality" story, with Oppenheimer upgrading on exactly that thesis (Yahoo Finance). The discriminator was half right. Cospecialization correctly picked the acquisition target: Globalstar got bought, while Iridium is itself buying Aireon, never a target. But cospecialization did not contain the re-rating: once the $17B mark existed, the sector-scarcity narrative lifted an uncospecialized holder anyway. The refinement we carry: cospecialization is necessary for the takeover premium, not for the re-rating. Separate those two questions in every future call, which is exactly what the live AST topic's control does.

The honest scoreboard. Resolved calls (1 and 2) at their blind confidences give a Brier of 0.130; the projected full four-call Brier at horizon, with the control firing, is 0.173. The control is most of the gap. A hindsight-flattered first cut of this same backtest scored 0.106 resolved and 0.109 projected, because it booked the control as a comfortable miss. Re-deriving blind, with the outcome excluded from the estimate, pushes the confidences down and the Brier up. The worse number is the point: it measures how much the original was flattered, and it caught a stale control read in the process. Backtest scores stay in their own lane, never mixed into the live record.

The chain

Every framework here traces to a named source in the strategy literature. The load-bearing ones are worth naming in the open, each tagged for whether we took it from the source or inferred the application.

- Elevating the constraint and throughput per constraint-unit. Eli Goldratt and Steven Bragg; drawn from source. The application, that buying the binding input both forecloses supply and publishes a mark, is our inference.

- Cospecialization and complementary assets. David Teece, Dynamic Capabilities; drawn from source. The reading that the takeover premium attaches to device-fused spectrum, splitting Globalstar from Iridium, is our application.

- Value network and cost structure. Clayton Christensen, The Innovator's Dilemma; drawn from source. The buyer-sorting (platforms buy, carriers rent) is inferred from value-network asymmetry.

- Increasing returns to adoption. W. Brian Arthur; drawn from source. The two-platform lock-in that compels the fast follower to secure the remaining supply is our application.

- Evolution stages and gameplay. Simon Wardley, Wardley Maps; vocabulary drawn from source, the land-grab reading of a constraint crossing custom-to-product inferred.

The full chain, every lens and graph node tagged drawn-from-source or inferred, lives in the prediction files, down to the signal. That is the method, run on a case where the answer is already known.

Related analyses

- Coverage Where the Towers End: the live D2D issue. This backtest froze the moment the platforms bought the spectrum; the live issue picks up after, when the carriers, boxed out of buying, pool and rent, and asks which adjacent layer catches the released margin. Both carry the same expected-miss control: the structure can be right while the equity that funds it fails to capture the gain.