The Constraint Is Not a Baton

"Power is the new AI bottleneck" is the sector's most crowded sentence, and the crowd draws two wrong conclusions from it. Three falsifiable calls: the chip premium holds, the equipment order books keep the rent, the power-stock trade is spent.

Strategic Structural Analysis · June 2026

The Call

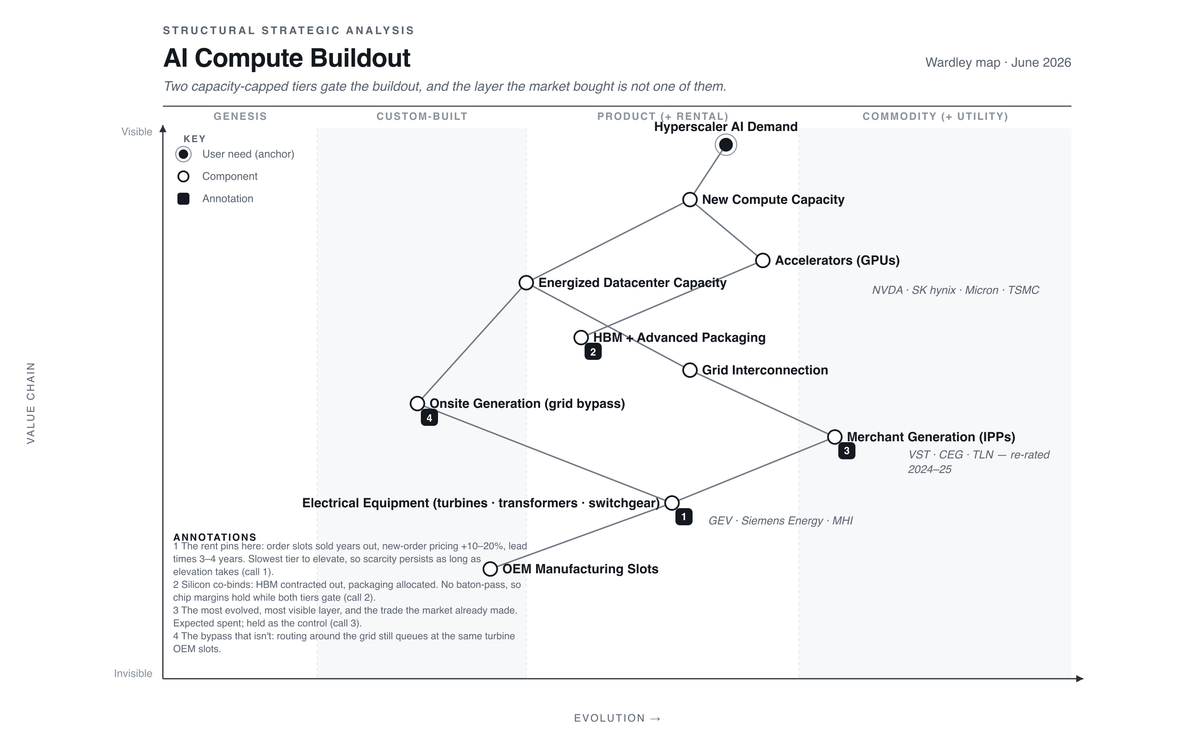

An AI datacenter needs two things nobody can rush: the accelerator chips that do the computing, and the electrical capacity that powers them. Both are rationed today. The chips queue behind high-bandwidth memory and advanced packaging, the two supply-capped steps that turn silicon into a sellable accelerator. The megawatts queue behind gas turbines, transformers, and switchgear with lead times measured in years. "Power is the new AI bottleneck" has meanwhile become the most crowded sentence in the sector.

The consensus draws two conclusions from that sentence, and we think both are wrong. The first is a relay: the constraint passed from silicon to power, so the chip premium should fade. The second is a trade: own the constraint by owning the power producers. Constraint logic, read carefully, says a system can hold two binding constraints at once. And it says rent persists not where the constraint is most visible, but where it is slowest to fix.

Read that way, this is a constraint that did not move. There is no clean handoff from silicon to power, because both inputs are slow to elevate and both keep their premium. That one claim is the spine of the three calls below.

This is a US-grid thesis: the binding constraint is US interconnection queues, PJM capacity auctions, and the lead times on equipment installed in the US. Siemens Energy (Europe) and SK hynix (Korea) enter as suppliers to US datacenter demand, not as their home markets — the grid buildouts in Europe and China run on their own constraints and are not what we are calling here.

We publish three falsifiable calls on that reading. Silicon and power stay co-scarce through 2027, so GPU (graphics processing unit) margins do not compress on a power-gated story (62%). The scarcity rent of the electrical-equipment tier, the turbine and transformer makers whose order slots gate every path to new megawatts, persists at or above its 2026 peak (78%). And a control, a call we publish expecting it to miss so the lens gets tested against the market's favorite trade (38%): that the independent power producers (IPP), the most visible constraint-owners, deliver another leg of outsized re-rating. The first two are structural claims the market is not pricing. The third is the trade the market already made, and we are betting it is spent.

The Situation

What happened, dated and sourced. The analysis comes after.

- 2025-12-15

Lawrence Berkeley National Laboratory's Queued Up survey counts more than 2,060 GW of generation and storage waiting in US interconnection queues, roughly twice the entire installed US fleet; the median project waits about 4.5 years (LBNL). - 2025-12-17

PJM, the largest US grid operator, runs its 2027/28 capacity auction and clears at the price cap in every zone ($333.44/MW-day), a region-wide shortfall (PJM BRA report). - 2026-02

Siemens Energy reports a record €154B order backlog and an all-time-high quarter of orders (€17.7B); book-to-bill, orders received over revenue billed, runs at 1.72, and the FY2026 outlook is raised (Siemens Energy Q1 FY26 release). - 2026-03-18

Micron's fiscal-Q2 2026 call: every calendar-2026 high-bandwidth-memory (HBM) price and volume agreement is already finalized, and new Singapore advanced-packaging capacity contributes meaningfully only from calendar 2027 (transcript). - 2026-04-01

Bloomberg reports more than half of US data centers planned for 2026 are expected to be delayed or canceled for lack of transformers, switchgear, and other electrical equipment (Bloomberg). - 2026-04-22

GE Vernova's Q1'26 results: gas-power backlog plus slot reservations grew from 83 to 100 GW in one quarter, with at least 110 GW expected by year-end; new orders priced 10–20% above the Q4'25 backlog; 25 turbines shipped (+32% YoY); guidance raised (GEV 8-K). - 2026-04-23

SK hynix's 1Q26 results: customer HBM requests exceed planned production capacity for the next three years, and customers prioritize procurement over price (SK hynix). - 2026-05-11

Wood Mackenzie's transformer survey, with PwC corroborating: standard large-power-transformer lead times run ~128 weeks, generator step-up units ~144 weeks, some orders out to four years (pv-magazine USA · POWER/PwC). - 2026-05-20

Nvidia's Q1 FY27 results: gross margin 74.9% under GAAP (generally accepted accounting principles), next quarter guided to 74.9% ±50bp, and $119.0B of supply commitments "strategically secured … to meet demand beyond the next several quarters" (NVDA CFO commentary). - 2026-06-05

The merchant generators re-rated hard into early 2025: Vistra +257%, Talen +215%, Constellation +91%, and "AI power stocks" comparison articles became a recurring retail genre. The June installment reports Constellation 25% down year-to-date through June 1 and Vistra 4% down (247WallSt 2026-01 · 247WallSt 2026-06).

The Mechanics

The dates fix the causal order, and it is not the order the headline implies. The prime mover is not the power scramble. It is hyperscaler demand hitting two inputs that were already slow to build. The equipment makers and the memory makers did not manufacture their scarcity; demand outran capacity that expands only on multi-year cycles, and the lead times were long before the narrative arrived. The grid scramble, the capacity-auction price caps, and the IPP re-rating are all reactions to that one collision, not the origin of it. So the question is not where the constraint went but which tier cannot be fixed inside the horizon, and who is in line for the fix.

Bottleneck: everyone found the constraint, few asked which tier is slowest to fix

The buildout's binding constraint is physical. You cannot energize a datacenter without transformers and switchgear, and you cannot add merchant megawatts without turbines. Eli Goldratt's constraint discipline says system throughput is set by whatever binds, and the headlines got that far. The question the headlines skip is the one the discipline actually turns on: not where the constraint is, but how long it takes to elevate.

Generation can be ordered. Equipment slots cannot be conjured, because the original equipment manufacturer (OEM) tier expanded capacity on multi-year cycles and its order books are the queue. The numbers say that queue is lengthening at rising prices: GE Vernova's backlog grew 17 GW in a single quarter with new orders priced 10–20% higher, and transformer lead times run near three years, stretching toward four.

Even the workaround confirms it. Hyperscalers routing around the grid with onsite generation land on the same turbine OEMs, in the same order books. Every path to a megawatt crosses an equipment slot. That is the first half of the constraint that did not move: power's binding edge is the equipment slot, and the slot is years from relief.

Mechanism: the rent of a binding constraint accrues to the tier that is slowest to elevate, and persists exactly as long as elevation takes.

No baton-pass: two constraints, one story, opposite trades

The consensus story is a relay. GPUs were scarce, now power is scarce, so the chip premium should hand the baton to the power premium. We call that assumed handoff the Baton-Pass: the relay reading of a constraint shift, in which a system carries one binding constraint at a time and relieving the old one strips its premium. Nothing in constraint theory licenses it. When two inputs are both slow to elevate, both bind, both keep their scarcity premium, and relieving one frees no throughput while the other still gates.

Silicon is still gated. All of Micron's calendar-2026 HBM supply is committed. SK hynix says demand exceeds planned capacity for the next three years. Advanced packaging, the assembly step that binds GPU and memory, stays allocated, and Nvidia has locked $119B of supply commitments to hold its place in the queue. When a stage of a value chain commoditizes, its profit moves to the adjacent stage that stays integrated; while nothing commoditizes, the profit stays put. That rule is the Law of Conservation of Attractive Profits, and it supplies the margin consequence here: while the accelerator-plus-memory stack stays integrated and scarce, its margin does not leak downstream to whoever owns megawatts.

The falsifiable version is one number. Nvidia's GAAP gross margin, guided at 74.9%, does not compress on a power-gated story. The strongest published version of the opposite view comes from the analyst who owns the equipment-tier pick: Tech Fund's May piece carries the frame "Nvidia is shipping. The gating constraint is high-voltage transformers, switchgear, and grid-tie batteries" (Tech Fund, 2026-05-09). We agree with them on equipment and take the other side on silicon, on the record, with a falsifier and a date.

Mechanism: co-scarce inputs hold their premiums simultaneously; a constraint shift strips margin only from the tier that actually stopped binding, and here neither did.

The spent constraint-owner: the map says the trade is over

Owning the obvious constraint-holder worked. Vistra, Constellation, and Talen tripled and doubled into early 2025 on exactly this narrative. The map supplies the discriminator: a layer this evolved, this legible, this talked-about is past the point of abnormal return. Once "AI power stocks" is a retail comparison genre, the narrative is consensus and the trade is over. The price action agrees: the comparison articles keep coming while Constellation sits 25% down on the year. The rent that remains sits two layers down, in the order books.

We hold this as a control prediction, expected to miss, and the precedent for humility is on our own scorecard: the same expected-miss structure said Iridium should not re-rate on a sector-scarcity narrative, and it has already fired, re-rating 193% (Yahoo Finance) ahead of its formal September 2026 resolution. A broad enough AI-power wave can lift already-priced names again. That is why the control sits at 38% rather than lower, and why it is a prediction rather than a dismissal.

Mechanism: a constraint that is consensus-visible is priced; the tradable residue migrates to the constraint tier the narrative hasn't reached.

Unit Economics: price the slot, not the story

Throughput accounting says to measure margin per constraint-unit, and the constraint-units here are concrete: a turbine order slot, a transformer delivery position, a packaging wafer start. Watch the price of the slot, not the revenue of the company. On the equipment side that is order pricing on a growing backlog, 10–20% higher at GE Vernova against a 100 GW book, which is the rent arriving years before it reports as revenue. On the silicon side it is GAAP gross margin holding near 75% while supply stays committed.

The wrong gauges are the headline ones. Equipment revenue lags the slot price by the length of the backlog. IPP equity prices carry the narrative, not the constraint. Two numbers give the first read on this issue's calls: GE Vernova's backlog and order-pricing language in late July, and Nvidia's margin print on August 26. Both probes are pre-registered below.

Mechanism: scarcity rent shows up first in the price of the constraint-unit, last in the income statement, and never reliably in the narrative equity, so the constraint that did not move can still strand the trade that bet it would.

The Predictions

1 · The equipment rent persists

Through 2027-12-31, the capacity-capped electrical-equipment tier (gas turbines, large power transformers, high-voltage switchgear) sustains its scarcity rent: order backlogs, lead times, and order pricing stay at or above their 2026 peak.

Confidence 78% · Horizon 2027-12-31

Wrong if: the equipment tier rolls over — gas-turbine and/or large-transformer backlogs shrink, lead times shorten materially below the 2026 peak, or OEM order pricing flattens/declines.

2 · No baton-pass

Through 2027-12-31, the constraint does not pass cleanly from silicon to power: GPU/accelerator supply stays co-scarce (HBM and advanced packaging allocated), so GPU gross margins do not visibly compress on a power-gated story.

Confidence 62% · Horizon 2027-12-31

Wrong if: GPU lead times collapse to commodity availability while power remains the cited gating factor, and accelerator gross margins visibly compress on that power-gated story.

3 · The obvious trade re-rates again (the call we expect to lose)

Through 2027-12-31, the merchant generators most associated with the AI-power trade (Vistra, Constellation, Talen) deliver further outsized, constraint-driven outperformance versus the broad market. We expect this to miss: the constraint is real but already priced into these names.

Confidence 38% · Horizon 2027-12-31

Wrong if (it hits): Vistra, Constellation, and Talen re-rate materially again on the power-constraint narrative.

Two probes resolve within weeks, pre-registered. GE Vernova's Q2 print (~July 21–23): gas-power backlog flat-or-up versus ~100 GW, with no pricing or lead-time rollover, at 85%. A hit lifts call 1 from 78% to about 84%; a rollover drops it to about 54%. Nvidia's August 26 print: GAAP gross margin at or above 72%, at 90%. A hit lifts call 2 from 62% to about 71%; a miss drops it to about 45%. Those updates were committed in the prediction files before any number lands. The probes are calibration instruments, scored in their own lane, never in the headline record.

Counter-signals, on the record. One shock breaks the first two calls through the same root: an AI-capex sentiment reset would pause equipment orders (call 1) and compress GPU margins for demand rather than power reasons (the stated adjudication risk on call 2: compression from competition or custom silicon muddies resolution either way). It would drop the IPPs too, resolving the control as a miss for reasons unrelated to what it tests. Elevation is slow, not impossible: the OEMs are adding capacity, and new slots could shorten lead times inside the horizon. On silicon, the 2027 Singapore advanced-packaging ramp is the clock on call 2: if it lands early and high-bandwidth-memory allocation loosens, the accelerator premium can leak before the horizon closes. And the control could fire: the Iridium precedent above shows crowded narratives get a second wind.

Every call lands on the public Scorecard when it resolves, Brier-scored at its authoring confidence. So far only backtest calls have come due — six, at a mean Brier of 0.155, where 0.25 is a coin flip — and they are labeled backtests, scored apart from the live record. No live call has resolved yet; when one does, you read it there.

The chain

Every framework here traces to a named source in the strategy literature; the load-bearing ones are worth naming in the open, each tagged for whether we took it from the source or inferred it ourselves.

- The system constraint and elevating it. Eli Goldratt, Theory of Constraints; drawn from source. The co-constraint reading, that two slow-to-elevate inputs bind simultaneously, is our inference.

- Throughput per constraint-unit, and the opportunity cost of the constraint. Steven Bragg, Throughput Accounting; drawn from source. Pricing the slot rather than the company is our application.

- Evolution stages. Simon Wardley, Wardley Maps; drawn from source. The discriminator, that a re-rated and well-understood layer is past the point of abnormal return, is our inference.

- Law of Conservation of Attractive Profits. Clayton Christensen & Michael Raynor, The Innovator's Solution; drawn from source. Its application to the accelerator stack is ours.

- Baton-Pass. Coined in this issue, extending Goldratt's system constraint: the relay reading of a constraint shift, which the theory never promises.

The full chain, every lens and graph node tagged drawn-from-source or inferred, lives in the prediction files, down to the page.

Related analyses

- Coverage Where the Towers End: the same conservation law, run in the opposite direction. There, rivals pooled a layer to commoditize it and the question was which adjacent layer catches the released margin; here, nothing commoditized at all, and the law's bite is that an integrated scarce stack keeps its margin. Both issues carry the same expected-miss control: being right about the structure is not the same as the obvious stock being the trade.