Coverage Where the Towers End

Direct-to-device puts a cell signal where no tower ever will. Three carriers just pooled the spectrum to deliver it — and released a profit pool in the process. Six falsifiable calls on who catches it.

Strategic Structural Analysis · June 2026

The Call

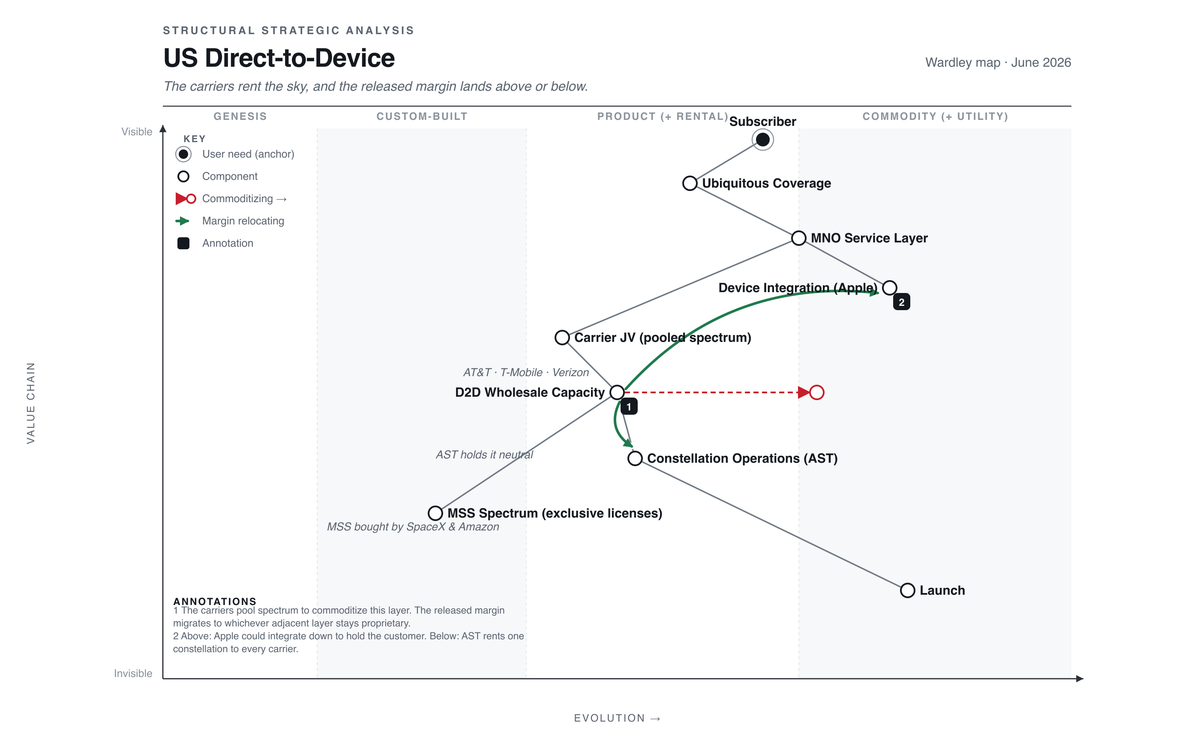

Direct-to-device means an ordinary phone connecting straight to a satellite, with coverage where the towers end and no special hardware in your hand. The US version is built on one stack by a short list of players: three carriers who own the customers (AT&T, T-Mobile, Verizon) and a handful of satellite operators who own the sky. The operators moved first. Through 2025 and into 2026, SpaceX and Amazon bought the scarce satellite spectrum outright and folded it into their own integrated stacks. Boxed out of buying at that scale, the three carriers agreed in principle in May 2026 to pool their own spectrum into a joint venture and rent capacity on equal terms.

That sequence has a structure, and the structure is the whole story. The carriers couldn't buy the sky, so they are renting it. Pooling a shared input commoditizes it, and when a layer of a value chain commoditizes, the profit that drained out of it does not vanish. It relocates to the adjacent layer that stays proprietary. Two layers sit adjacent to commoditizing carrier capacity: the constellation below, where AST SpaceMobile rents to every carrier as a neutral supplier, and the device above, where Apple could integrate down toward the satellite. The released margin lands on one of them.

We bet it lands below, on the neutral host, and that the carriers being forced to rent rather than own is exactly what keeps that host independent. This is a US thesis: US carriers, US-licensed satellite spectrum, US regulator. Rakuten in Japan and Vodafone in Europe appear only as minority shareholders in AST, not their home markets, and their regions are not what we are calling here. We publish six falsifiable calls on where the margin lands, whether the neutral host holds the slot, and whether the platforms that forced the JV stay out of the carriers' channel, at confidences from 42% to 72%, most resolving in the twelve months to mid-2027.

The Situation

What happened, dated and sourced. The analysis comes after.

- 2025-09-08

SpaceX agrees to buy EchoStar's AWS-4 and H-block satellite spectrum for about $17B, locking up scarce, hard-capped licensed airwaves under a single buyer (EchoStar IR). - 2025-11

SpaceX adds EchoStar's AWS-3 spectrum portfolio for about $2.6B, extending the same lockup (EchoStar IR). - 2026-04-14

Amazon agrees to acquire Globalstar for about $11.6B, a roughly 117% premium, folding its global mobile-satellite licenses into Amazon's Leo platform; Globalstar is also the backend behind Apple's iPhone Emergency SOS, so that relationship moves to Amazon too (CNBC). - 2026-05-13

AT&T, T-Mobile, and Verizon agree in principle on a satellite D2D joint venture: pooled spectrum, shared standards, broader access for "satellite providers." An agreement to cooperate, not a signed deal, with no definitive terms, no financial structure, and no timeline yet (Advanced Television). - 2026-05-14

ASTS rises about 12% to $83.66 the next day, and AST publicly commends the proposed JV, welcoming the deal rather than fearing it (StockTitan). - 2026-05-28 → 06-08

ASTS runs to an all-time high of $133.86, then falls to about $93.60 on Blue Origin launch-partner concerns and stretched valuation. The market has settled on direction; it is still arguing over level (MacroTrends). - 2026-Q1

AST reports about $3.5B cash, nearly 60 carrier agreements covering roughly 3B subscribers, FY2026 revenue guidance of $150–200M, about 45 BlueBird satellites targeted in orbit by year-end, and a 98.9 Mbps peak to an unmodified phone: fast enough to prove the physics, on far too few satellites to sell at scale yet (Q1 2026 8-K).

The Mechanics

Bottleneck: the scarce input is licensed spectrum, and the carriers can no longer buy it

A satellite can only transmit on airwaves a regulator has licensed it to use. That spectrum is the binding input: hard-capped by physics, rationed by the FCC, and the one thing in this chain you cannot manufacture more of. In 2024 the FCC's Supplemental Coverage from Space rules opened a second path, letting satellites borrow a carrier's terrestrial spectrum to reach a phone (FCC). Either way, the input is a license, and licenses are scarce by law, not by convention.

Watch who moved on that input. SpaceX paid about $17B for EchoStar's satellite spectrum, then about $2.6B more. Amazon paid about $11.6B for Globalstar. Two vertically integrated platforms bought the scarce input outright and folded it inside their own stacks. By the time the three carriers sat down in May 2026, buying their way to a spectrum position at that scale was no longer on the table. The platforms had taken it.

So the carriers did the other thing buyers do when they cannot own a constraint: they pooled. Pooling spectrum and standardizing the interface is the move that turns a scarce input into a shared, rentable one. It is the tower-industry playbook re-run, where carriers once built tower networks together and then sold them to neutral owners they all rent from today.

Mechanism: when you cannot buy the constraint, you commoditize it, and renting a shared layer is how three rivals do that without handing any one of them the keys.

Margin migration: renting the sky moves the profit, it does not destroy it

Here is the rule the whole issue turns on. When one stage of a value chain commoditizes, the profit that used to live there reappears at the adjacent stage that stays proprietary and interdependent. Christensen and Raynor named it the Law of Conservation of Attractive Profits, and it is the single most useful rule for predicting where margin goes next. Profit is conserved. It relocates rather than vanishes.

Apply it to the carriers' forced move. By renting the sky instead of buying it, the three carriers commoditize the capacity layer they sit on. The margin that layer used to hold has to go somewhere adjacent and still proprietary. Two layers qualify. Below sits constellation operations, where one operator's satellites can serve every carrier at once. Above sits the device, where the chipset and the operating system meet the customer. The released margin migrates to whichever of those two stays integrated and hard to copy.

The layer below has a feature the layer above does not. AST's constellation is cospecialized with a coalition: nearly 60 carrier agreements and no single anchor tenant. We call that Coalition Cospecialization, and it is the difference between AST and Globalstar. Globalstar was tied to one anchor, Apple, and got bought. An asset locked to many mutually distrustful buyers at once is worth most when it stays neutral, because control by any one carrier would devalue it for all the others. The many-partner lock is what protects independence. The carriers renting rather than owning is the same fact seen from their side.

The device layer is the live rival claimant, and the timing rule says to expect it to try. While direct-to-device is still not-good-enough, integrated plays win, so a vertical-integration attempt from the device is exactly what the good-enough timing rule predicts. Apple owns the device, the operating system, and the customer, and pre-funded a constellation once already. But the device and the constellation feed different channels. Apple's stack is cospecialized for the consumer it sells phones to, not for the carrier-wholesale pool the JV just created, and its old satellite backend now belongs to Amazon.

Mechanism: renting the sky relocates the released margin to the layer that stays proprietary, and the neutral constellation is proprietary in a way no single carrier can capture.

Unit economics: the neutral host collects rent the integrators cannot

Run that forced move through a P&L. A rural cell tower costs about $250k to serve a few dozen people (dgtlinfra). For the dead zones past the last tower, that math never closes, which is why the coverage was never built. D2D competes against nonconsumption there, against no service at any price, not against a rival network. The market it opens is new, not stolen.

The neutral host's edge is that it sells the same constellation to every carrier. One set of satellites, many tenants, each carrier's subscribers covered without AST building anything carrier-specific. Increasing returns compound it: each carrier coalition that signs lowers AST's cost per covered subscriber and raises the next coalition's incentive to rent rather than build its own. An integrator captures one customer base. A neutral host captures the rent on all of them.

That same capital intensity is the catch, and it is why one of our calls is a control we expect to lose. Building the constellation is slow and expensive. AST holds about $3.5B in cash but raised more than $1.0B in new debt last quarter and spent about $379M on equipment and spectrum (Q1 2026 8-K), and the satellites are mostly unbuilt. The operating layer can win the rent while the equity that funds the build absorbs the gain through dilution. By contrast, T-Mobile's Starlink D2D service already ships at about $10 a month (T-Mobile), proof the consumer price point is real while AST is still proving it can serve it at scale.

Mechanism: renting the sky is the move the carriers had left, and collecting that rent at falling unit cost is the neutral host's reward, but the rent reaches the operating layer first and the equity only after the build is paid for.

The Predictions

1 · The carriers rent, they don't buy

Through 2027-06-30, the AT&T/T-Mobile/Verizon satellite JV (and its members, individually or collectively) will not acquire majority control of AST SpaceMobile; the relationship resolves as commercial wholesale procurement, at most with continued minority investment.

Confidence 70% · Horizon 2027-06-30

Wrong if: by 2027-06-30 the JV or its member carriers (individually or in aggregate, per public filings) hold or have agreed to acquire >50% of AST's voting equity or its US operating business.

2 · The neutral host consolidates the slot

By 2027-06-06, AST remains independent (no change of control) and signs at least one additional carrier-collective capacity arrangement, either the US JV's definitive wholesale agreement or an international multi-carrier analog. Both legs must hold.

Confidence 55% · Horizon 2027-06-06

Wrong if: by 2027-06-06 either (a) a change of control of AST is agreed or announced (any acquirer: carrier, platform, SpaceX), or (b) no new carrier-collective capacity arrangement (US JV definitive agreement or international multi-carrier deal) has been signed.

3 · The JV stays multi-vendor

By 2027-06-06, the JV's definitive arrangements are operator-neutral: no single satellite operator, AST included, wins exclusivity over the pooled spectrum or the JV's D2D procurement.

Confidence 72% · Horizon 2027-06-06

Wrong if: by 2027-06-06 the JV's announced definitive terms grant a single satellite operator exclusive rights to the JV's pooled spectrum or exclusive D2D supplier status.

4 · The structural winner is not the trade (the call we expect to lose)

Through 2027-06-30, ASTS equity delivers a sustained, outsized re-rating attributable to its neutral-host consolidation, materially outperforming a satellite/comms benchmark off the strength of calls 1 through 3 playing out. We expect this to miss: the mechanism can be right while the capital-intensive equity, already sharply retraced from an all-time high, fails to capture it by this horizon.

Confidence 42% · Horizon 2027-06-30

Wrong if (it hits): by 2027-06-30 ASTS delivers a sustained outsized re-rating clearly attributable to the neutral-host thesis, materially outperforming a satellite/comms benchmark, without that gain being erased by a dilutive raise, a launch-execution setback, or a valuation de-rating.

5 · The device layer does not capture the channel

Through 2027-06-30, Apple neither acquires or takes control of a satellite-constellation operator nor launches a paid consumer D2D data service beyond emergency/SOS that bypasses the carrier-wholesale channel. Mainstream consumer D2D stays carrier-delivered over neutral-host capacity, not device-bundled by Apple.

Confidence 60% · Horizon 2027-06-30

Wrong if: by 2027-06-30 Apple (a) acquires or takes control of a satellite-constellation operator, or (b) launches a paid consumer D2D data service beyond emergency/SOS that delivers mainstream connectivity outside the carrier-wholesale channel, or (c) the device layer otherwise demonstrably captures the released carrier-D2D wholesale margin.

6 · The platforms don't bypass the channel

Through 2027-06-30, the integrated platforms that forced the JV (SpaceX/Starlink and Amazon Leo, which own their spectrum and full stacks) do not capture mainstream US consumer D2D by going direct to consumers and bypassing the carrier-wholesale channel. Mainstream D2D stays carrier-delivered, including carrier-resold platform capacity like T-Mobile's Starlink service.

Confidence 62% · Horizon 2027-06-30

Wrong if: by 2027-06-30 an integrated platform (SpaceX/Starlink or Amazon Leo) sells, or announces with a firm launch date, a mainstream paid consumer D2D data service in the US sold direct to consumers (not via a carrier wholesale arrangement) to standard handsets; emergency/SOS-only and enterprise or IoT niches do not count.

One probe resolves within weeks, pre-registered. AST's Q2 print (around August 10–17) tests call 1's distress leg: FY2026 revenue guidance held at or above $150M and no control-changing carrier transaction, at 78%. A hit nudges call 1 up; a guidance cut or control event drops it. That update was committed in the prediction files before any number landed, and it is scored in its own checkpoint lane, never in the headline record.

Counter-signals, on the record. The cleanest break runs through capital. AST's own capital intensity could force a control-changing equity raise despite its cash, flipping calls 1 and 2 through the same root, and the same dilution is why we expect the equity control to win even as the structure plays out. Apple is the genuine blur risk: it holds the strongest integration position on the board, owns the customer, and could acquire a constellation outright, which is exactly the move that breaks call 5. But the sharpest threat to the whole thesis is the prime mover itself: SpaceX or Amazon could skip the carriers and sell D2D direct to consumers, hollowing out the wholesale channel the neutral-host slot depends on. That is call 6, and a fast move there pressures calls 1 through 3 at once. And crowded narratives get a second wind: our own backtest control said Iridium should not re-rate on a spectrum-optionality story, and it re-rated +193% year-to-date (Yahoo Finance) before resolving. That precedent is why call 4 sits at 42% rather than lower.

No live call has resolved yet; when one does, it lands on the public Scorecard, Brier-scored at its authoring confidence, backtests labeled as backtests.

The carriers couldn't buy the sky, so they're renting it. That forced move hands the released margin to the operator no carrier can own, and our bet is that the landlord is the constellation below, not the device above. Being right about that structure is not the same as owning the right stock, which is why one of these six calls is the one we expect to lose.

The chain

Every framework here traces to a named source in the strategy literature. The load-bearing ones are worth naming in the open, each tagged for whether we took it from the source or inferred the application ourselves.

- Law of Conservation of Attractive Profits. Clayton Christensen & Michael Raynor, The Innovator's Solution; drawn from source. The two-claimant application, constellation versus device, is our inference.

- Cospecialization and complementary assets. David Teece, Dynamic Capabilities; drawn from source. Coalition Cospecialization, the many-partner lock that protects a neutral host where a single anchor invites a buyout, is coined here, extending Teece.

- Increasing returns to adoption. W. Brian Arthur; drawn from source. The application, that each carrier coalition lowers AST's cost per subscriber and raises the next coalition's incentive to rent, is ours.

- Commoditization versus centralization, and the value chain. Simon Wardley, Wardley Maps; vocabulary drawn from source, the rent-don't-buy reading of the JV inferred.

- Elevating the constraint and throughput per constraint-unit. Eli Goldratt and Steven Bragg; drawn from source. The control framing, that the capex to build the constellation funds ahead of the revenue it unlocks, is our application.

The full chain, every lens and graph node tagged drawn-from-source or inferred, lives in the prediction files, down to the page.

Related analyses

- The Constraint Is Not a Baton: the same conservation law, run the other way. There an integrated, scarce stack keeps its margin because nothing commoditized; here three rivals deliberately commoditized a layer and the question is which adjacent layer catches what they released. Both issues carry the same expected-miss control, testing whether the structural winner is also the tradable one.